The currently flat oil market has caused some worry among oil-exporting countries with sluggish prices since the second half 2014, leading the Organization of Petroleum Exporting Countries (OPEC) to take stage, deciding to curtail the output by 1.2 million barrels per day in November, which was again renewed in May in association with non-OPEC producers. OPEC's decision to cut production for the first time in eight years brought the end of the free oil market and re-introduced market management. However, since the prices are still struggling to reach $50, the cartel's decision raised questions regarding market rules for the "black gold."

Speaking to Daily Sabah about pricing dynamics and the impact of OPEC decisions, IEA oil market analyst Olivier Lejuene said that output and demand are the main driving force of the oil market, adding that prices are expected to continue to drive the market in the next few years.

"OPEC decisions can move prices up and down for up to several months, but in the end, the economics of production and demand always re-assert themselves," Lejeune noted, saying the situation has gained clarity in recent months as OPEC's initial decision brought prices up by $10 before increased production of shale and other products took prices back down in March. "Prices are now back to where they were before the OPEC agreement, and traders are calling for 'more cuts' in order to support prices," he said.

On July 11, 2008, oil prices hit historic high at $147.27 per barrel over the last couple of days, fueling speculation on future oil trade contracts. At the time, most experts said that market speculation alone was unlikely to have such a profound impact on commodity prices, leading to a reaction from the OPEC that led the U.S. Commodity Futures Trading Commission (CFTC) to launch an investigation into future contracts, ultimately coming to the conclusion that manipulation did not have a striking impact on prices but was rather driven by market conditions where supply failed to meet the demand of the rapidly growing global economy of decades' prior.

Market dynamics have always existed, and in the said period, the basic rules of economics were at play. Markets were struggling to find equilibrium between supply and demand. Unstable circumstances surrounding oil production in Nigeria, the result of workers' strikes and terror attacks, had a major impact on supply, as the African country that had formerly been one of the biggest oil producers in the world with a capacity to produce 2.6 million barrels per day (b/d) - coupled with the crisis in Iraq - led to a considerable drop in supply. On a similar note, the labor strife and nationalization in Venezuela where Exxon Mobil shut down production registered a significant decline in supply, as well.

While the oil and gas sector saw its heyday during the first half of 2008, the sector fell in the second half of that year due to one of the world's biggest recessions, triggered by the collapse of financial markets that sent oil prices plummeting below $40. Again in 2011, after the market recovered from the recession and the price of "black gold" hovered between $90 and $100 until the second half of 2014, when the profound increase in U.S. oil production - coupled with low demand from emerging economies - brought about an oil glut. By February 2016, oil was trading below $30 with China experiencing a slowdown in economic growth.

Plunging oil prices spoiled the budgetary expectations of all producers, not only for national companies attempting to fulfill social and political obligations but for companies in the private sector, as well. For instance, export-based revenues declined to $450 billion in 2016 as opposed to $1.2 trillion in 2012.

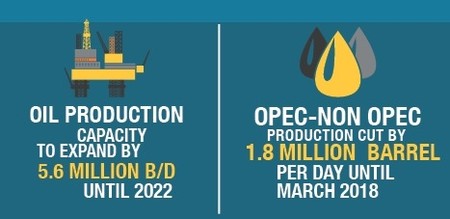

In November 2016, OPEC agreed to curtail production to support prices, for the first time since 2008. In the aftermath of the oil giants' meeting in Vienna, oil was trading well above $50. Later in May, OPEC and non-OPEC producers decided to extend the production cut until March 2018 by 1.8 million b/d. The effect of the OPEC decision does not, however, seem to have pushed prices further upward as oil has been trading below $50 for more than a month due to expanding stocks in the U.S. Once again, market dynamics primarily based on the law of supply and demand have worked themselves out. It is, however, necessary to emphasize that the impact of cuts in output cannot be assessed immediately as production from non-OPEC countries, particularly in the U.S. as well as cut-exempt OPEC countries like Nigeria and Libya, is increasing. This multidimensional facade of oil production explicates the declining or flat crude prices, experts put forward.

Oil demand to increase by 1.2M b/d each year until 2022

Today, the market has been characterized as volatile and dominated by specific uncertainties. The Oil Market Report 2017 released by the International Energy Agency (IEA) outlines both analysis and forecasts through the year 2022, highlighting that the price outlook is not static although investors do not expect supply to be overrun by demand.

According to calculations by the international energy watchdog, global oil and gas upstream investment declined by 25 percent in 2015 and by another 26 percent in 2016. A modest recovery has been observed regarding 2017 investments, facilitated by increasing investments in U.S. shale oil and cost reductions. "When the investment market does recover, it will serve an industry that is far leaner and fitter than it has ever been; one that will be able to deliver more with less," the IEA said, pointing to the role of investments in sustaining equilibrium in the industry.

Examining the ongoing projects and the likelihood of their delivery, the IEA suggests that towards the end of the five-year period, little recovery is expected in liquidity to aid prices."Our analysis suggests that, unless additional projects are given the green light soon, towards the end of our forecast horizon - 2022 - we will be in a 104 million b/d market, and the call on OPEC crude oil and stock change rises from 32.2 million b/d in 2016 to 35.8 million b/d in 2022. The group expects to add 1.95 million b/d to its production capacity in this period, which implies that available spare production capacity will fall below 2 million b/d."

This numerical explanation of the IEA suggests that the oil market will tighten and price expectations will increase. Yet, if new projects are added to the list of current ones in OPEC and non-OPEC countries and concerns about a low spare capacity are eased, then the existing flat curve of the future of crude will prove resilient. If no projects are added, the curve will take an upward turn, although there is no definite projection regarding price increases.

As demand is also expected to rise based on the 2-million-b/d demand growth in 2015 and 1.6 million b/d in 2016 due to colder-than-normal temperatures and higher demand from industrial fuel users, the IEA has revised is expectations for global oil demand. The agency says it will keep growing at an average of 1.2 million b/d each year until 2022.

During a session at the 22nd World Energy Congress, IEA Chief Executive Dr. Fatih Birol presented the latest report on World Energy Investments, saying that the IEA believes that oil demand will continue to grow, albeit at a slower but steady pace.

Oil production capacity expand by 5.6M b/d by 2022

Highlighting the steady growth in demand, the IEA oil market report also elaborates on the supply side, supported by the increase of serious oil production in the U.S. "We believe that by the end of 2017, LTO production will be approximately 500,000 b/d higher than it was one year earlier. Even in a world where oil prices do not move substantially above $60, light tight oil production will continue to grow through 2022, adding 1.4 million b/d over the period," according to the report. It also indicated that Brazil, Canada and Kazakhstan were added to the list of areas where output increase will occur, with cumulative output rising 2.2 million b/d by 2022, reaping the rewards of investment decisions taken before oil prices declined.

"Growth is heavily front-loaded and supply looks ample through the early part of the forecast. Unless further projects are sanctioned quickly, growth will all but stall from 2020 onward," the IEA oil market report said, emphasizing the necessity for more investments to avoid the jeopardy of a steep surge in crude prices towards the end of 2022.

Reiterating the unpredictable situation in Libya where a modest rise in prices has been observed, the majority of growth will come from major producers in the Middle East, which will contribute an estimated 1.79 million b/d to the total growth in OPEC's production capacity, according to the agency's statement that also states that global oil production capacity is forecast to expand to 5.6 million b/d by 2022, as a potential price recovery tempts producers to invest after two slow years. However, the statement also stresses that actual production and production capacity are two different things.

With regards to supply expectations, IEA oil market analyst Lejeune stated that the IEA continues to expect global oil stocks to draw returns in the second, third and fourth quarters of 2017 as demand increases above supply.

"A big factor of uncertainty in our forecast is production in countries that are not part of the OPEC agreement, such as Libya, Nigeria and the U.S. The main question on everyone's minds is the current pace of destocking," Lejeune said as they continue to speculate whether it will be enough to bring stocks down substantially, since the market wants to see it happen before up-bidding the price.

Stressing the fact that the current oil market is ruled by bears, Dr. Cyril Widdershoven, the founder and director of the Dutch-based Integrated Risk Consultancy firm Verocy, emphasized that most analysts and investors are currently only looking at perceived negative issues with regards to oil prices.

"As long as we are only looking at oil stock volumes, combined with the increased number of rigs in the U.S., the sentiment will stay large to expect lower price settings. However, when looking at market fundamentals, most lights are green, as demand is up, geopolitical risk is up and the global economy is still showing overall growth."

Highlighting that the perceived additional oil volume on the market is still very questionable, Widdershoven drew attention to the intractable dynamics overshadowing production operations in conflict-torn regions such as Iraq, Nigeria and Libya.

"Iraq, Nigeria and Libya are stated as countries where more oil is going to be produced soon. The latter totally depends on their internal security issues, which are currently under pressure," he said while stressing that a crisis between the Kurdistan Regional Government (KRG) and Iraq's central government could lead to a loss of volume. Drawing attention to the fact that the future of Libya remains in the balance since it was torn apart in conflicts and Nigeria is exposed to risks as Niger Delta groups continue to target production facilities.

Widdershoven's emphasis on internal and regional security issues facing oil-producing countries further substantiates claims regarding the role of political stability and security in the maintenance of supply and demand curves. So long as the security risks continue and no one is able to guarantee otherwise, the supply side of equilibrium will be exposed to certain threats. Yet, there always seems to be some sort of compensation for the loss of supply, as the U.S.'s somewhat serious oil production is forecast to keep its momentum; a point that Widdershoven says cannot be missed. He also claims that the production of shale oil will experience pressure or perhaps even put on hold in several oil fields in the U.S., as shale oil production per well has been on the decline in recent months.

Investments in oil and gas upstream operations have declined for two years in a row compared to investments in energy efficiency, which have increased, leading Widdershoven to opine that if overall financing moves to other sectors, oil production will be curtailed even further. He strongly emphasized that, given current oil market forecasts and taking into account various elements that affect supply and demand, the only way for prices to go is up.

At a time when demand is expected to increase, production is under pressure and OPEC will keep to its own production cuts despite exemptions and refusal of non-OPEC members like Kazakhstan, which produces 1.6 million b/d and has recently announced that it wants a gradual exit from an OPEC-led deal on oil production curbs and a rise in output one or two months after its expiration.

In the context of this complicated picture, it seems that basic market rules will take over. In this case, if geopolitics were to also play a role in production operations and supply were unable to outstrip demand growth, then prices will be pushed upwards, despite lack of consensus regarding when.